GRIDTECH, an international exhibition and conference, provides a platform to manufacturers, suppliers, academicians, and consultants to exhibit their state-of-the-art technologies, products, and expertise and to get exposure to the emerging technologies in the fields of transmission, distribution, smart grid, renewable integration, energy storage, electric vehicle charging infrastructure, communication, etc. As usual, this year’s GRIDTECH, which was held during 3rd to 5th April 2019, enjoyed a considerable amount of success. Organized by Power Grid Corporation of India Limited (POWERGRID), with the support of Ministry of Power, Government of India, and in association with CBIP and IEEMA, GRIDTECH 2019: 6th International Exhibition and Conference, attracted many manufacturers, suppliers, academicians, and consultants.

Need for Sustainable and Environmental-Friendly Energy

Vice President of India

In his keynote address, Mr. Venkaiah Naidu, Hon’ble Vice President of India, said that in view of the increasing demand in the power sector with each passing day, it was necessary to fully tap the potential for sustainable and environmental-friendly energy. He said there was a need for finding new technologies to harness renewable energy in a big way.

According to Mr. Naidu, India has made an international commitment to de-carbonize electricity generation. Towards this end, India has set a time-bound target of installing 175 GW of renewable generation by 2022, comprising 100 GW solar, 60 GW wind and 15 GW of other forms of renewable generation. With the focus increasingly shifting to clean energy in recent years, India has become an attractive destination for investments in the renewable energy sector.

Mr. Naidu also said that adequate growth in renewable energy would serve dual purpose– firstly, it would contribute towards achieving energy security to the nation and it would address the environmental concerns, which needed to be tackled on a war-footing.

Phenomenal Growth of the Power Sector in India

Ministry of Power

Highlighting the phenomenal growth of the power sector in India in the past few years, Mr. Ajay Kumar Bhalla, Secretary, Ministry of Power, said that India had reached the installed capacity of more than 350 GW which included about 36 percent capacity coming from non-fossil fuel resources such as wind, solar, and hydro. He also said that peak energy shortages had now come down to below 1 percent owing to the record electricity generation capacity and transmission facilities and that by sending the transmission network especially to the inter-regional capacities, India had ensured that there were no constraints in transmission of power from one part of the country to another. According to Mr. Bhalla, India had been striving to achieve One Nation-One Gird-One Market and making concerted efforts to ensure electrification of all the villages. He claimed that the target to electrify all the villages was met last year and that the country had nearly achieved electrification of 100 percent households. The country’s next target was to ensure 24×7 reliable power supply to all, he added.

Indian Power Sector – A Perspective

One of the highlights of GRIDTECH 2019 was the presentation given by Ms. Seema Gupta, Director (Operations), POWERGRID, on the Indian power sector.

According to Ms. Gupta, the Indian power sector has evolved from local/state grids in local areas to regional grids. When we realized that regional grids were no longer sufficient, we went for national grids. We are now moving towards global grids with an increased focus on IoT, cyber, software, and digital applications. The basis of this evolution is increased societal expectations, growing economy, and sustainability of the power sector.

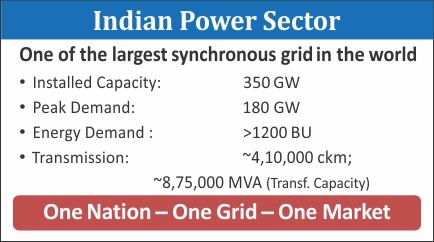

Ms. Gupta said that “the Indian power sector is one of the largest synchronous grids in the world with installed capacity of 350 GW, peak demand of 180 GW, and energy demand greater than 1200 billion units (BU). We also have transmission lines of more than 410,000 circuit kilometer (ckm). Today’s Indian power sector can boast of having a One Nation-One Gird-One Market.”

Exponential Growth of the Indian Power Sector

In the past 5 to 10 years, the Indian power sector has grown exponentially with 113 GW generation capacity added between the years 2014 and 2019. In this 113 GW generation capacity, the private sector’s participation in growth has been 73 percent and the overall share of private generation in installed capacity has touched 46 percent (about 161 GW). The overall share of generation in the installed capacity of the Central sector is 24 percent and the State sector is 30 percent.

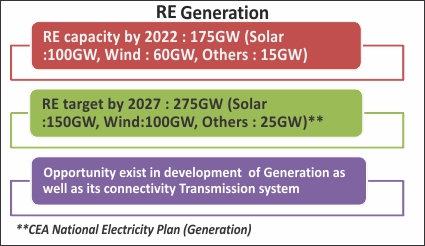

Along with this growth, there has been a changing pattern in generation source as well. Fossil fuel resources are becoming constant, fluctuating from 64 percent to 68 percent and again back to 64 percent from 2008 to 2019. The low-capacity addition in hydro resources has led to a decline in the generation share from 22 percent to 13 percent. While at the same time, the share of renewable energy has increased from 7.70 percent of 143 GW installed capacity in 2008 to 21 percent of the overall 350 GW capacity in 2019. At present, a total of around 75 GW of renewable energy (RE) capacity has been installed in the country. The goal is to reach 175 GW of renewable energy capacity by 2022, which includes 100 GW from solar, 60 GW from wind, 10 GW from bio-power, and 5 GW from small hydro-power.

Along with this growth, there has been a changing pattern in generation source as well. Fossil fuel resources are becoming constant, fluctuating from 64 percent to 68 percent and again back to 64 percent from 2008 to 2019. The low-capacity addition in hydro resources has led to a decline in the generation share from 22 percent to 13 percent. While at the same time, the share of renewable energy has increased from 7.70 percent of 143 GW installed capacity in 2008 to 21 percent of the overall 350 GW capacity in 2019. At present, a total of around 75 GW of renewable energy (RE) capacity has been installed in the country. The goal is to reach 175 GW of renewable energy capacity by 2022, which includes 100 GW from solar, 60 GW from wind, 10 GW from bio-power, and 5 GW from small hydro-power.

As transmission plays a vital role in transmitting the generated capacity, there has been an accelerated growth in transmission reaching about 1,53,000 ckm (added since 2012). This big increase stems from addition in the higher capacity network, that is, 765kV AC and 800kV (HVDC) transmission lines. The 765kV transmission line was around 5000 circuit kilometers in 2012, which increased to 41000 ckm in 2019.

Besides extending our network to every nook and corner of the country, we have extended the transmission system to neighboring countries like Bhutan, Nepal, Bangladesh, and Myanmar; and there is plan to link Myanmar and Sri Lanka as well. The cross border inter-connection capacity is around 3060 MW, and we expect that it will increase to 6700 MW in the next two years. Most of the lines are under construction.

Indian Power Sector Outlook

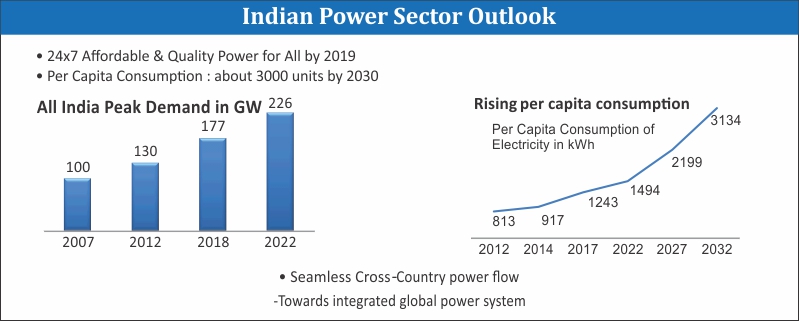

The per capita consumption is around 1100 units, and India aims to reach 3000 units by 2030. The all India peak demand is expected to touch 226 GW by 2022. We are targeting to add 1,10,000 ckm transmission line length with over 3,80,000 MVA capacity coupled with the green energy corridor to facilitate the evacuation of power from renewable resources. We will be investing an estimated INR 2,70,000 cr. for the Indian power sector’s growth in the next five years.

During the period of growth, there has been various disruptions and changes in the power sector, such as non-fossil-fuel-based generation, distributed generation, multi direction power flow focusing on transfer of power from both the sides, right of way and constrained land for substation, rapid urbanization, large inter-connection area, more focus on automation and digitalization, increased use of electricity to meet energy requirement, and short gestation period of RE. We are constantly looking for solutions to resolve the problems related to the power sector.

We are moving towards high voltage lines from 400kV to 765kV with 1200kV in the development stage. The HDVC line was 500kV but two links have been added for the 800kV lines and the hybrid network development. To increase the capacity of transmission corridor, HTLS conductors, FACTS (SVCs/STATCOMs), and shunt and series capacitors are put into use. To take care of urbanization, we are optimizing the tower design. We are also implementing the first cable and VSC-based HVDC lines in Kerala under right of way and constrained land for substation. There will be more and more use of GIS substations, automation, and wide area measurement.

India has about 7 bipole HVDC system lines which are under operation. One bipole is under construction. We will also build a VSC control system which is expected to come up in another one year’s time. During the initial development of the Indian power sector, all the regions had different frequencies. All these regions were connected with HVDC back-to-back lines, and we still have four such lines that have proved to be quite useful for grid operators in managing the power flow of AC lines. We have 14 hybrid STATCOMs; out of these eight have already been commissioned and three have been commissioned partly. To increase and balance the power flow over the parallel corridor, 48 FSC/TCSC have been commissioned.

Asset Management

Many technological innovations have been done under asset management. We have established a National Transmission Asset Management Centre (NTAMC) which can control all the stations from a centralized location. To support these stations, we also have 10 Regional Transmission Asset Management Centres (RTAMC) and from the network of about 242 substations, 192 substations can be remotely operated and maintained from RTAMCs and NTAMC; and In a big way, we are moving forward with the implementation of substation automation system.

In the 765kV vertical data configuration, the earlier tower had a requirement of 85m, making it quite huge. Gradually, we started designing compact towers and now we are using 64m for 765kV S/C. However, in the Indian power sector, we are now mainly using the 765kV D/C lines. There was a time when the 765kV transmission system in the Indian power sector was in accordance with the development taking place in the rest of the world.

Once there was a concern about the monitoring/patrolling of the transmission lines which was generally done by the manual staff. The concern was about whether it was done in the right manner, how to have a legacy reports or are correct measures being taken to rectify the issues. To counter such issues, we developed a piece of software called Patrosoft. This software records all the data in a tablet, and the patrolling staff visits the tower to activate the data. The personnel sitting in the office can monitor and access the data such as legacy reports, generation of analytical reports, evaluation of manpower performance, regulation of patrolling-based financial claims, and optimal utilization of patrolling manpower.

Patrosoft is an ideal tool for utilities that are engaged in transmission asset management. We also make use of the drone over lines for carrying out the patrolling to detect the defects and rectify later. Moreover, apart from using Patrosoft, we make use of high-zone cameras that allow the staff to click pictures and use them to detect defects. We are also using helicopters in areas that are inaccessible and can cover 100 to 150 kms in a day. Although, there are certain restrictions as we need get clearance from the defence department before using the data or making it public. In one of the lines, when we analyzed the data shots taken from the helicopter, there were some clearance issues between the conductor and the metallic lines. This can be very handy in rectifying the problem and tripping to be reduced to great extent.

Patrosoft is an ideal tool for utilities that are engaged in transmission asset management. We also make use of the drone over lines for carrying out the patrolling to detect the defects and rectify later. Moreover, apart from using Patrosoft, we make use of high-zone cameras that allow the staff to click pictures and use them to detect defects. We are also using helicopters in areas that are inaccessible and can cover 100 to 150 kms in a day. Although, there are certain restrictions as we need get clearance from the defence department before using the data or making it public. In one of the lines, when we analyzed the data shots taken from the helicopter, there were some clearance issues between the conductor and the metallic lines. This can be very handy in rectifying the problem and tripping to be reduced to great extent.

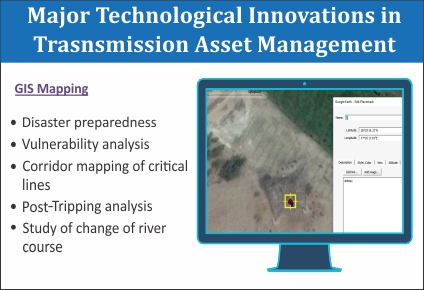

We are also using GIS mapping of transmission lines to keep in check the vulnerability of the line in case the river course changes and we are able to take precautionary measures in few of the lines where the tower is about 100 m to 150 m from the river course, but due to change in the course of the river the tower becomes vulnerable. On the basis of GIS mapping, we can take corrective actions in time and shift the lines to the safe zone. We can also check the post-tripping analysis to find the reasons behind the occurrence of change in the river course. GIS mapping is extensively used in known areas where there are incidents of change in the river course.

Digital Substations

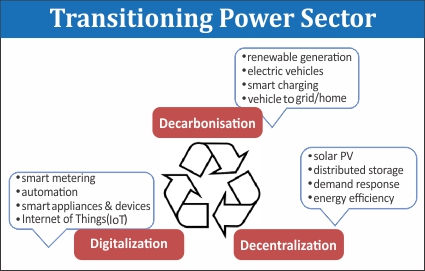

As we move towards more renewable and advanced generation, we have to start adopting digitalization and automation. There are substations with thousands of copper cables running the scheduling, and we can use the pilot project having the process optimization technology, where the entire signal from various units is coming through the fiber. The implementation time can be cut down because the entire signal can be transmitted. The tracing of the fault becomes easy – one can easily detect the fault in fibers. Moreover, the fire hazards can be minimized if there are any such accidents. We will be implementing digital substations in our new substations and will be using this new technology as a step towards digitalization. The countries that are witnessing growth are emphasizing highly on de-carbonization and decentralization moving towards distributed generation and digitalization which covers smart metering, automation, IoT, etc. India is also focusing on these three areas.

As mentioned earlier, in renewable integration we are targeting 175 GW by 2022 and 275 GW by 2027. We are also focusing on smart grids and e-mobility with plan to have 15 percent of electric vehicles of all vehicles sales over the next five years. After completing the mission to connect each house in India with electricity, we will be moving towards providing 24×7 affordable quality power for all.

As mentioned earlier, in renewable integration we are targeting 175 GW by 2022 and 275 GW by 2027. We are also focusing on smart grids and e-mobility with plan to have 15 percent of electric vehicles of all vehicles sales over the next five years. After completing the mission to connect each house in India with electricity, we will be moving towards providing 24×7 affordable quality power for all.

RE Generation and Transmission Business Opportunity

Moving ahead, what kind of opportunities is available for stakeholders as far as renewable integration, investments or the requirement in transmission is concerned? Opportunity exists in the development of generation and its connectivity transmission system. India has installed capacity of 75 GW; and to meet the target of 275 GW, we need to add 200 GW more by 2027. Looking at the broad estimate, the investment requirement for the power sector generation will be around INR 9,00,000 cr., INR 1,20,000 cr. in transmission, and INR 40,000 cr. for dedicated transmission system to cater to the renewable addition in the power sector.

Moving ahead, what kind of opportunities is available for stakeholders as far as renewable integration, investments or the requirement in transmission is concerned? Opportunity exists in the development of generation and its connectivity transmission system. India has installed capacity of 75 GW; and to meet the target of 275 GW, we need to add 200 GW more by 2027. Looking at the broad estimate, the investment requirement for the power sector generation will be around INR 9,00,000 cr., INR 1,20,000 cr. in transmission, and INR 40,000 cr. for dedicated transmission system to cater to the renewable addition in the power sector.

There are certain challenges in the renewable integration of such a large quantum not just in India but the world over. As per our findings, there are four areas that we need to address for facilitating large scale RE integration – smart technology/digitalization, energy storage, increase balance area-cross county connections, and policy initiatives/regulatory interventions.

Smart Technology

As we already know, for digitalization we have to give more visibility to operators. We have started the use of AMI, PMU, and weather sensing and measurements to prepare the operator and the grid in advance to take care of issues occurring in renewable integration. We are now moving more towards IT-based solutions such as ERP, GIS, CRM, etc., and OT like substation automation, field automation, and SCADA. The increasing use of these technologies facilitates the integration of such a large quantum of renewable energy. Moreover, communication and security are also playing a vital role in the renewable integration process. It has become an important factor in power system operations, and for all communication systems fiber optic is put in use. There are wireless sensors network and integrated communication security implemented in the system now. Control and management centers are being set up across the nation. We are setting up 11 renewable energy management centres (REMCs) for better scheduling and estimating forecasting tools. The renewable energy generators can set up their own forecasting tools and aid power system operators to analyze how RE generation is going to be integrated into the grid.

Looking at the RE capacity penetration by 2027, about 44 percent of generation is expected to come from renewable energy, which is 21 percent as of now. This expected capacity generation will impact grid stability. The grid needs to be prepared in order to take care of surging requirements. As per an estimate, the balancing requirement in India will be 24000 MW/hour in a 15-minute block. We have to get balancing and ramping support from flexible resources coupled with energy storage techniques. When renewable energy goes out of the system, we will be required to ramp up balanced generation at a fast pace.

Energy Storage System

In energy storage, India is expecting a requirement of about 40 GW by 2042 and investment requirement of around INR 38500 cr. in the energy storage techniques in the power sector to have the type of response in renewable generation India is looking for.

When we talk about increasing the balancing area, the Indian power sector is quite connected with the neighboring countries. Another major step is to increase the area in South Africa and Europe. In addition, India has to ensure that it connects Central Asia, SAARC countries. As per the report, there is a high potential of solar energy in Central Asia (1700 GW) and Iran (750 GW). Iran is also rich in natural gas (66 GW) while Mekong countries are heavily dependent on Hydro (30 GW). If these regions can be integrated, there will be synergy in the generation.

If we look at the diversity in demand and energy availability, there is a latitude span of about 45°E to about 109° E (Span of 64°) from Vietnam to Iran. India can take advantage of different time availability of solar generation and the demand curve. As per the estimate, peak hours for Vietnam (Eastern Most) and peak hours for Iran (Western Most) would have a time difference of about 4.30 hours. If we can connect these countries, the advantage of having different peak hours and energy availability will facilitate two directional power flow and the countries that are having low demand can supply renewable energy to places where demand is higher. Interconnection of countries will allow optimal utilization of resources.

With correct policies in place, India could facilitate a rapid integration of 175GW renewable energy by 2022 and 275GW by 2027. Policy interventions have been done starting from the Indian Electricity Act, 2003, which emphasized on the development of grid interactive renewable power, tariff determination, renewable purchase obligation, grid connectivity, and market development. The National Electricity Policy, 2005, focused on competition and development of RE technologies and provided for a policy for the repowering of wind power projects (August 2016) and competitive bidding and guidelines for grid connected solar PV power projects (August 2017). The Tariff Policy, 2016, provided for solar RPO to be 8 percent by 2022, and smart meters to be mandated to take care of distribution side management. In India, there are no transmission charges for solar and wind power. These RE resources are commissioned before a certain period and do not include transmission charges. The countries that are looking forward to moving towards large scale renewable integration, policy, and regulatory interventions would be a key factor.

At the regulatory level, the issues related to the deviation charges of RE generators have been delinked from frequency. Now each renewable generator knows its obligations. Moreover, the commercial liability is now known and upfront with no additional charges and surcharges. People with sufficient renewable generation can have renewable energy certificates (RECs) to ensure physical energy balance. Centralized (LDCs) and de-centralized (generators, aggregators) forecasting is now available.

As per the Indian Electricity Grid Code, 55 percent of flexibility in conventional generation has been provided to renewable generators. The implementation of deviation settlement mechanism has provided better provisions for states that are rich in renewable energy; these states are given a larger band so that there are no penalties. India has also started ancillary services operations, which have turned out to be a great boon for ramping-up and ramping-down requirements and which offer a roadmap for operationalizing the reserves. At the forum for regulators, issues such as harmonization of accounting and settlement systems of various intra-state grids were raised.

Some of the policy interventions have been implemented while some of them are still in the pipeline. Policies such as the intra-state settlement system and imbalance handling, forecasting (Load/ RE generation/ net load, spinning reserves, frequency control (primary/secondary/ tertiary), technical standards for RE generation, ancillary services, balanced portfolio, flexibility – harnessing and incentivizing, market design enhancements, communication in the power sector, and capacity-building of all stakeholders are being progressively implemented. The focus is on developing policies and regulations for these areas to address the prevalent concerns.

Way Forward – What Lies Ahead?

What is the way forward? According to Ms. Gupta, the way forward will be a coordinated national effort for development of transmission, generation, and load. It is important to have assessment of load by each state, coordinated planning, and implementation in a collaborative manner. If we want to move more towards renewable energy, transmission has to lead generation. Coming to technology, automation of substations, centralized and remote operation of substation, focus on energy storage, and smart grid applications should be given more importance. The other important area is augmentation of balanced area by having cross-country interconnections.